Re: Entering the EMU - not such an easy task? - a reply on the Baltics

Dejan - just some follow-ups from my side on your post:

As for this article its part of a more broad discussion of whether the NMS are suitable for euro adoption. The issue that immediately springs to my mind is the discussion of whether the Maastricht criteria (MC) can fulfill their original task of assessing this. I am quite surprised that this discussion does not focus upon the relevance of the MC in judging it, though I guess looking form the potential entrants point of view – the criteria are taken as given, thus a major change is not an issue. What about a minor change, or not even a change in the criteria, just a small degree of flexibility on the issue of when to evaluate?

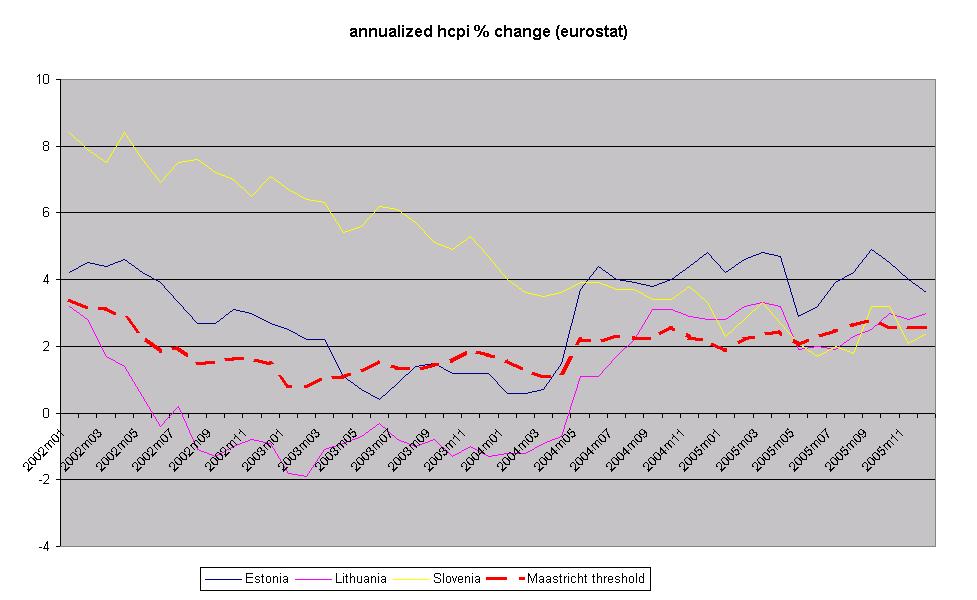

Generally the EMU is experiencing quite low levels of inflation at the moment, which causes the benchmark to be relatively low compared to previous years. I have recalculated the Maastricht entry value for December 2005 data for annualized rate of inflation of the HCPI, and therefore will use the obtained 2.6% as the Maastricht entry requirement. Despite the exact values may differ, I will use the ones I calculated to explain some of my points. So, assuming the 2.6% as the cut-off value, if the evaluation was to take place on the 1st of January 2006, Estonia (3.6%) and Lithuania (3%) would not be eligible for the Euro entry, while Slovenia(2.4%) would have made it, at least on this criteria, by a small margin.

I suppose the objective of the MC on inflation, aside of course “proving” that a countries economy is stable, is to limit the inflation differentials within the union. Putting aside the issue of whether inflation is somewhat of an endogenous entry criteria, we should first note, that the MC methodology uses inflation rate for the three lowest inflation countries in the EU to calculate this cut-off value. And which were these in December 2005? Poland, Finland and Sweden – of which two are not in the EMU, and do not seem to be determined to enter. If we recalculate the benchmark using only EMU members data (which would arguably serve better to look at differentials in the union) we obtain the benchmark value of 3.1% which is already more favorable for or countries of interest. Second, if we look at the annual inflation rates for the countries already in the EMU – the examples of Greece(3.5%), Spain (3.7%) and Luxembourg(3.4%) prove that differentials of similar magnitude already exist within the common currency. Estonia, has an economy so small, that we can hardly imagine its inflation rate to be disruptive for the monetary policy of the EMU, and thus banning its entry on this ground is hard to justify, especially when a country as large as Spain, with a similar inflation rate, already exists within the union.

Third, all three countries in question, especially the Baltic two, have a sound fiscal situation (in terms of the MC criteria on debt and deficit), and I see no reason (despite the political one of course) that Italy and Greece with huge debt burdens and a tradition of high fiscal deficits, saw these criteria somewhat overlooked when the judgment was made and entered (eventually) the EMU, while the Baltics may be excluded do to scrutiny on differentials on a variable, that I can not imagine more important more important than the differentials of Italy and Greece with respect to criteria on the fiscal variable.

There was an article by W. Munchau in the FT about a month ago claiming that Estonia and Lithuania are too poor to join the Euro, and that it will be too costly for them. I do not want to go too deep into arguing against this (which I will when I find the article) but I disagree with the whole argument of being too poor for the emu – especially that for countries with a long tradition of fixing currencies, one can hardly expect them to enter at an overvalued rate.

Will Estonia and Lithuania be made a favor by the EU of being reviewed when they find it appropriate?

The idea (at least allegedly) of the MC was to assess the convergence and its stability of the economies in question. As in the article, the position of the Baltics of setting a favorable evaluation date and hoping for a one-off fulfillment is against this idea. But this even further strengthens the argument against the MC – together with the past experiences of Greece, Italy and others – we can clearly see fulfilling it does not guarantee anything, especially that there is always some room for adjusting (manipulating?) the figures.

First, I do not see any reason for excluding them from the Eurozone, especially that both countries have maintained currency boards for over a decade, surviving crises and for the last years pursued fixing to the euro itself. They have a sound fiscal policy, and by default performed well on the exchange rate criterion.

Second, as I explained before the inflation criteria is flawed.

Third, precisely because of the currency boards they follow, there is not much these countries can do about inflation – especially that their fiscal policy is already quite tight, and reserve requirements on banks are among the largest in Europe.

Moreover, denial of entry at an expected date could put an additional strain on the economy – Estonians seem more aware of that, as the voices of postponing entry seem to be louder than in Lithuania. The credit boom in these countries may anyway go bust, but if it goes bust inside the EMU the consequences should be less disruptive, as the credibility of the currency tie would be of a different order of magnitude.

Overall, I would in favor of allowing the Baltics to enter – there seem to be benefits, hardly any costs for both sides, and a small obstacle as marginal mal-performance on one entry criteria should not be used to hold them outside.

Finally, contrary to the authors, I would not claim that Slovenia is on the safe side – solely looking at the enclosed graph (inflation rates) show us that it is not far from the border value, things could change, and its adoption of the euro could potentially be jeopardized, especially if the numbers are looked at with too much scrutiny.

posted by tomasz kozluk @ 7:46 PM

1 comments

![]()

![]()